FTA has come up with a new public clarification no. 3 Manpower vs Visa facilitation services 8 (Manpower vs Visa Facilitation Services), which can resolve one of the challenges faced by UAE companies in the application of VAT.

This clarification arises in the instances where an employment visa is held by one company while the employees work under the supervision and control of another company.

There are two kinds of supply which having different VAT treatments in this scenario. Therefore, it’s necessary to identify the supply for applying the correct VAT treatment: Manpower Services or Visa facilitation services.

Let’s understand in detail for each of these supplies and its treatment under VAT.

Manpower Services

When a Company (Supplier) identify/recruit/hire the candidates and make such employees available to another Company (Customer), then it is generally regarded as a taxable supply of manpower services under the VAT legislation.

Here, the Supplier is generally responsible for all the employment obligations, including the payment of salaries and other benefits. Besides that, the Supplier will be responsible for ensuring whether the employee has performed their duties and the quality of work as well.

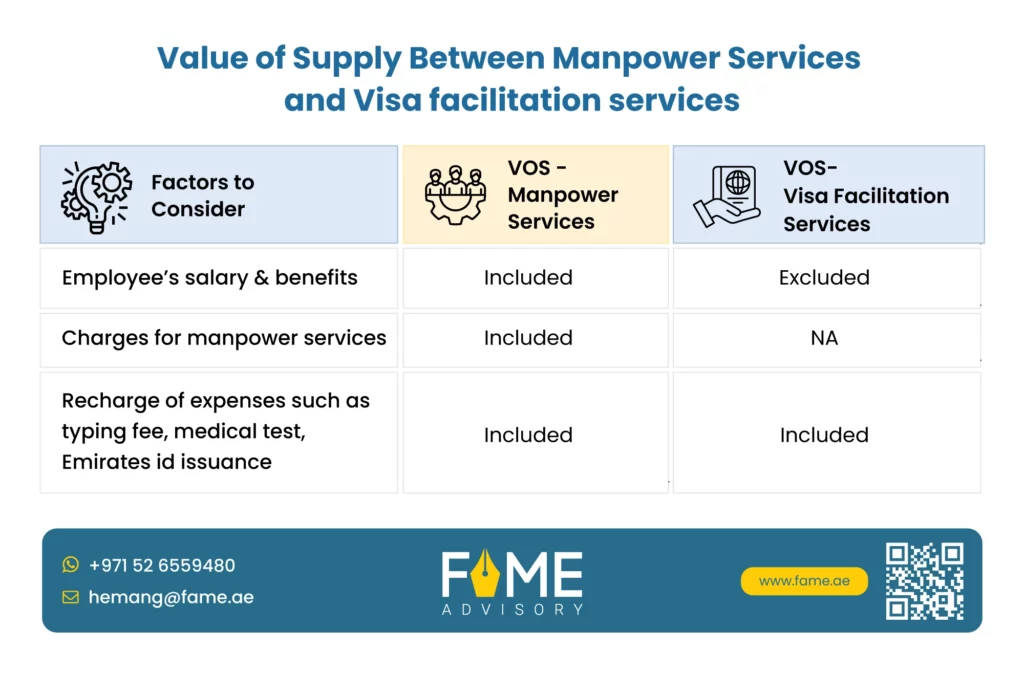

Value of supply: Consideration includes the full amount received or expected to be received by the Supplier from the Customer, including employees’ salaries, benefits, or any additional amount charged and other recharges related to manpower services.

I.e., Consideration = Salaries & other benefits paid to employee (whether paid by Supplier/Customer)+ any additional amount charged by the Supplier respect to this supply

Visa Facilitation Services

This is like an exception to manpower services. A supply would not be treated as a supply of manpower services but instead, as a supply of visa facilitation services when all the following conditions are satisfied:

1.The employment visa holder (“Facilitator”) and the Customer are part of the same corporate group but are not part of the same tax group. (If it is under the same tax group then such supply would be out of scope in VAT)

Here, a question arises: what is the corporate group?

These are companies operating in the same corporate structure, which includes common ownership of the companies specified under clause (2), article (9) of Executive Regulation.

2. The Facilitator’s business activities do not include the supply of manpower.

This means if the facilitator supplies any manpower services to any person the condition will not be met.

3. The facilitator is not responsible for any of the obligations related to the employee

As a part of visa facilitation, customers take responsibility for the following obligations:

- Payment of an employee’s salary.

- Payment of other monetary benefits, including financial incentives, annual flight allowances, and housing allowances.

- Provision of medical insurance and accommodation

So, the customer has to pay all these employee obligations.

And facilitator’s obligation is limited to incurring the cost relating to obtaining the employment visa

4. The Facilitator sponsors these employees to exclusively work for and under the supervision and control of the Customer.

Implies that employees exclusively work for the Customer and are under that Customer’s supervision and control, this condition would be met.

If any of the conditions above fail to be met by the facilitator, then such supply shall be treated as a supply of manpower services

Nature of Supply: Visa facilitation services are also regarded as taxable supply in UAE

Value of Supply: Value of facilitation services differ from value of manpower services

Here Value of supply = amount changed for the services which could include the recharge of expenses such as typing fees, medical tests and issuance of employee Emirates IDs

The value of the supply of visa facilitation services excludes the employee’s salary, annual flight allowance, and any other monetary benefits, as these are the obligation of the customer.

In short, what FTA trying to differentiate here is the value of supply between these two services i.e. manpower Vs visa facilitation services, which can be summaries below;

Special valuation rule for supply between related parties & supplies without any consideration

Value of Supply – Related parties

Case-1: The facilitator charges a fee that’s equal to the market value of the supply, The fees charged would be regarded as consideration for the taxable supply of services, and that will be the value of supply.

Case-2: The facilitator charges a fee that is less than the market value, then the value of supply is the market value of the supply; the facilitator is required to impose VAT on the market value of the supply, regardless of the actual amount charged for the visa facilitation services.

Value of Supply – No fee is charged

When supply happens without any consideration, the provisions of the deemed supply will trigger.

However, if the supplier has not recovered the input VAT for the related goods or services, a supply made by him without consideration will not be regarded as deemed supply (Article 12 of VAT decree-law).

When a Facilitator provides facilitation services to customers without charging any fee there are two possible scenarios

Case 1: If the facilitator does not recover the input VAT incurred to make the supply, then the supply of visa facilitation services will not be deemed supply. It would fall outside the scope of VAT.

Case 2: The facilitator recovered any input VAT tax to supply the visa facilitating services, the facilitator will be required to account for the output tax due based on the total cost incurred to make the supply, including direct and indirect costs.

(Here “direct cost” refers to costs that specifically relate to the services provided within this context, including typing fees, logistics, and any other fees charged for the purpose of visa issuance. “Indirect costs” refers to overhead expenses (e.g. office rental and utilities) as well as other general operational expenses incurred by the Facilitator).

In instances where the Facilitator is unable to calculate the cost of providing the visa facilitation service, the market value of similar services may be used as an indication of the value of the supply.

Examples for Manpower vs Visa facilitation services

Supply of Manpower Services (Example 1)

Company A holds the employment visas for employees working at Company B. Company A makes these employees available to Company B. Hence, Company A is regarded as supplying manpower services irrespective of whether the employees’ salaries and benefits are paid by Company A or Company B.

The consideration for the supply of manpower services is equal to the total amount incurred by Company B, including salaries and benefits (irrespective of whether the employees’ salaries and benefits are paid by Company A or Company B), as well as any amounts related to the services provided by Company A to Company B in relation to the supply of the services.

Supply- Exception to Visa Facilitation Service (Example 2)

Company A holds employment visas for persons working for Company B. Company A and B are part of the same corporate group.

As part of Company A’s operations, it also provides secondment services to businesses outside its corporate group. Company A is, therefore, regarded as supplying manpower services, and the supply does not meet the second condition.

Consequently, the supply of visa support services provided by Company A to Company B does not qualify as a supply of visa facilitation services and Company A is regarded as supplying manpower services to Company B.

Uncover the difference between Manpower services and Visa facilitation services

Define your employment visa supply status with us.