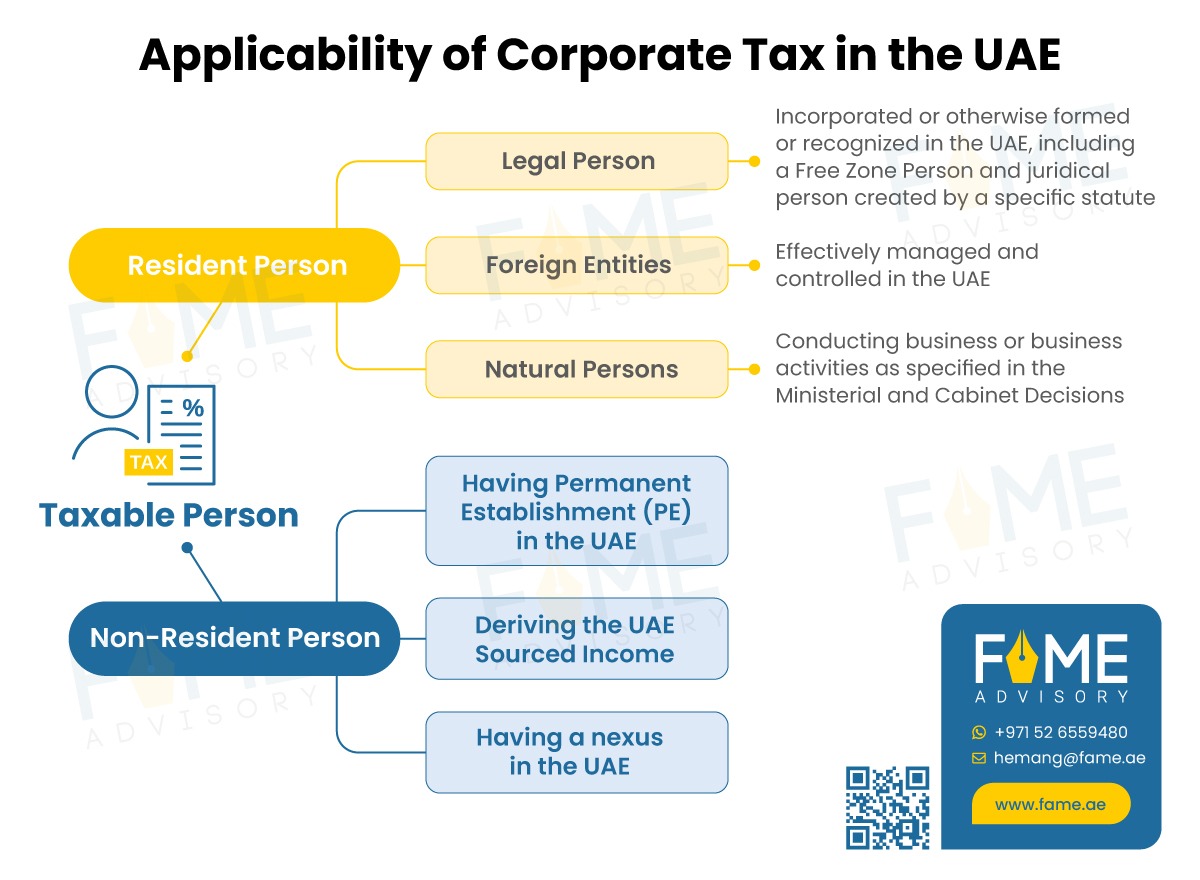

Applicability of Corporate Tax in the UAE

The UAE Corporate Tax regime came into force for taxable persons for financial periods starting on or after 1st June 2023. The UAE CT applies uniformly to all seven Emirates. The corporate tax provisions apply to all UAE companies and other legal entities performing business activities with some exceptions.

The taxable persons subject to UAE Corporate Tax are:

1. Resident Person who can be:

- A Legal person incorporated or otherwise formed or recognised in the UAE, including a Free Zone Person and juridical person created by a specific statute (e.g. by a special decree). A foreign entity being managed and controlled in the UAE.

- An individual who conducts a business or business activity in the UAE as specified in the Ministerial and Cabinet Decisions.

2. Non-Resident Person who either has a:

- Permanent Establishment (PE) in the UAE; OR

- UAE-Sourced Income; OR

- Nexus in the UAE