The Advance Pricing Agreement (‘APA’) programme offers a voluntary mechanism for a Person to enter into an agreement for determining the Arm’s Length Price of Controlled Transactions over a period of time and preventing the risk of TP disputes and litigation.

APA is an agreement by the Authority with a Person, which sets the criteria to determine the Arm’s Length Price in relation to Controlled Transactions entered or to be entered by that Person with its Related Party/Parties, over a fixed period of time.

Key Benefits of an Advance Pricing Agreement

- Predictability

- Facilitated collaboration

- Reduced Disputes

- Prevention of double taxation

- Prevention from risk of TP disputes

- Streamlined compliance

Key Aspects of an Advance Pricing Agreement

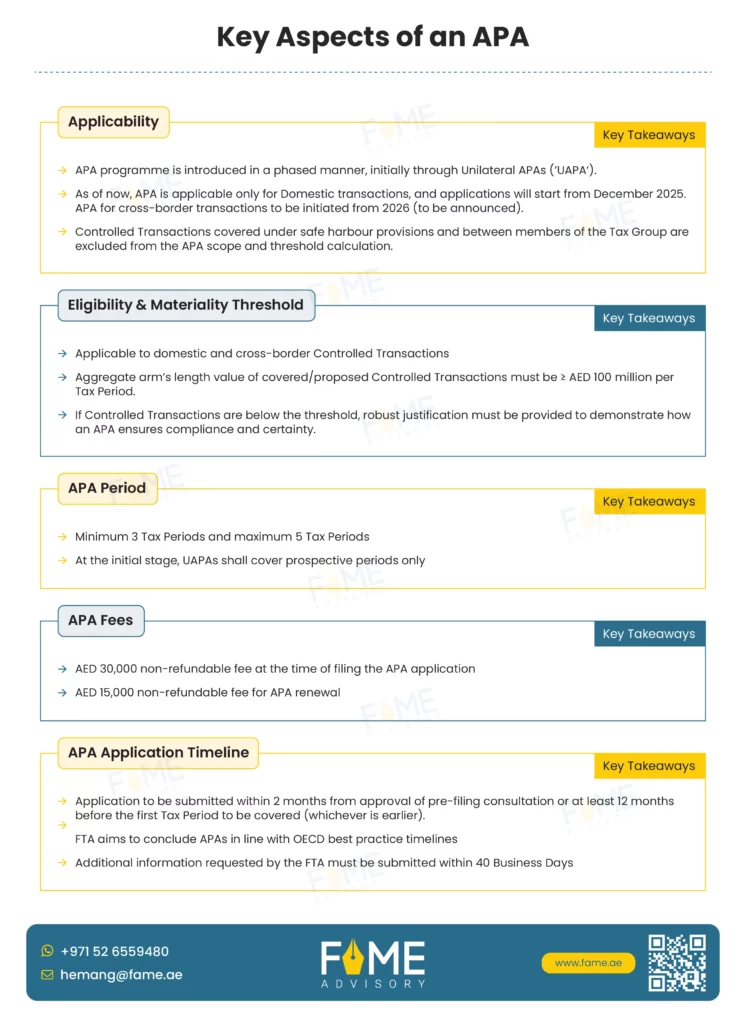

- Applicability

- Eligibility & Materiality Threshold

- APA Period

- APA Fees

- APA Application Timeline

Types of APAs:

An APA can be of the following types:

- UAPA: A UAPA is an agreement between a Person and the FTA for domestic and cross border Controlled Transactions. The UAPA shall be binding only on the FTA, and the Person that is a party to the UAPA, to provide tax certainty exclusively from a UAE Corporate Tax Law perspective. The UAPA is not binding on any foreign taxpayer or foreign tax administration that may be the counterparty to the Controlled Transactions covered by the UAPA.

- Bilateral APA (‘BAPA’): A BAPA is an agreement between competent authorities of two jurisdictions reached through a MAP. A BAPA provides tax certainty in relation to Controlled Transactions in the UAE and the relevant foreign jurisdiction.

- Multilateral APA (‘MAPA’): A MAPA is a set of agreements between competent authorities of more than two jurisdictions reached through a MAP.

Stages of APA

Stage 1 – Pre-filing consultation

A Person proposing to enter into an APA must make a request to the FTA for a pre filing consultation. The purpose pre-filing consultation is to enable the FTA and the Person to understand the possibility of entering into an APA. Only a Tax Agent registered for Corporate Tax purposes with the FTA can submit the APA Request on behalf of the Person in the prescribed form. Communication with the FTA on the APA programme can be submitted from 30 December 2025. FTA aims to conclude pre-filing consultations within 6–9 months of receiving the request.

A pre-filing consultation does not bind the FTA to enter into an APA and does not constitute an APA application. The FTA may reject a Person’s request, for any of the following reasons:

- Indication of a tax avoidance strategy

- Limited scope of APA

- ALP can be determined beyond significant doubt

- Forecast of significant restructurings

- Unsatisfactory rationale to include Transactions

- Unpredictable business

Stage 2 – Filing of an APA application

A Person may submit an APA application upon receiving notification to proceed. The application must be filed within 2 months of the FTA notification or at least 12 months prior to the commencement of the first Tax Period to be covered under the APA, whichever is earlier.

Indicative UAPA timelines (assuming January – December as the tax period)

APA pre-filing | APA pre-filing approval by FTA (assumed as six months) | APA application | APA covered tax periods |

|---|---|---|---|

1-Jan-2026 | 30-Jun-2026 | 31-Aug-2026 | 2028-2032 |

1-Apr-2026 | 30-Sep-2026 | 30-Nov-2026 | 2028-2032 |

1-Jul-2026 | 31-Dec-2026 | 28-feb-2027 | 2029-2033 |

The FTA may reject an APA application under certain circumstances, including but not limited to:

- Materiality threshold not met

- APA doesn’t cover pre-filing consultation issues

- Significant discrepancies between contracts and actual business

- Changed Circumstances or Delayed Responses for requested information

- Analysis is inadequate or unreliable

- Application contains wrong or misleading information.

Stage 3 – Evaluation and negotiation

Once site visits, interviews, meetings, and the collection of all required information and documents are complete, the FTA will commence its evaluation and analysis. FTA shall prepare a Transfer Pricing analysis that addresses manner and key criteria of determining ALP, any other terms and conditions, including critical assumptions

The Person must provide written feedback on the FTA’s TP analysis within 30 Business Days. The FTA may allow a discussion of the TP analysis upon the Person’s request. If no mutual agreement is reached after negotiations, the APA may be closed without conclusion, with no refund of fees.

Stage 4 – Conclusion and Implementation of APA

The FTA shall discuss the implementation of the agreement with the Person. The FTA and the Person shall sign the APA agreement based on terms mutually agreed. A Person may withdraw an APA application anytime before conclusion. Withdrawal without valid justification, especially at an advanced stage, is discouraged. No refund of fees will be provided.

An APA is binding on signatories to the APA with respect to the Controlled Transactions for the Tax Periods covered under an APA. APA does not establish a precedent for any other Tax Periods of the Person, nor for any other Person that is not covered under the APA.

Advance Pricing Agreement Annual Declaration

A Person with an APA agreement must file an APA Annual Declaration for each covered Tax Period, in the format prescribed by the FTA. The APA Annual Declaration must be filed by the later of the following:

- Within 90 Business Days of signing the APA, or

- The due date for filing the Tax Return.

Revision, Cancellation, Revocation of APA

FTA May Revise an APA under following circumstances:

- Change in UAE Corporate Tax affecting Controlled Transactions.

- Change in business, economic, or other conditions requiring reassessment of critical assumptions.

- Exceptional circumstances notified by the Person.

If revision is not feasible or no mutual agreement is reached, APA may be cancelled prospectively from the Tax Period in which the event occurred, remaining valid for prior periods.

FTA May Revoke or Cancel an APA under following circumstances:

- Material misrepresentation in APA application or Annual Declaration.

- Failure to comply with material terms and conditions.

- Breach of critical assumptions.

APA may be revoked from the first Tax Period covered; previously governed Controlled Transactions become subject to Corporate Tax Law and Tax Procedures Law. Depending on severity, FTA may cancel APA prospectively, starting from the Tax Period of breach and applying to subsequent periods.

Renewal of APA

Application of renewal of APA may be made by the Person if there are no material changes to facts of the Controlled Transactions and the critical assumptions remain valid.

Renewal application shall be made at least three months before the expiry of the existing APA. Renewal request shall follow same procedures as filing of APA application, with the exception that a pre-filing consultation is not required.

In Conclusion: Advance Pricing Agreement

The APA programme provides an effective framework for achieving transfer pricing certainty and minimizing disputes by allowing taxpayers to agree in advance on arm’s length pricing for Controlled Transactions. With clearly defined eligibility criteria, timelines, and compliance requirements, APAs promote predictability, transparency, and alignment with OECD best practices. For eligible taxpayers, the programme serves as a valuable tool to manage transfer pricing risks and ensure sustained compliance under the UAE Corporate Tax regime.

Search

Recent Insights